Abstract

Being a sovereign currency, CBDC has special advantages over central bank money, such as integrity, trust, safety, and liquidity. Among other reasons, lowering operational costs associated with physical cash management, promoting financial inclusion, bringing resilience, efficiency, and innovation to the payments system, enhancing the efficiency of the settlement system, fostering innovation in cross-border payments, and giving the general public access to uses that private virtual currencies can offer without the associated risks are the main reasons for investigating the issuance of CBDC in India. In rural areas, using CBDC’s offline capability would be advantageous because it would increase availability and resilience even in the absence of mobile service or electricity. The Reserve Bank of India (RBI) pilot of its central bank digital currency launched and joined a small cohort of central banks researching central bank digital currencies (CBDCs) that have advanced past the conceptual stage to the pilot stage. This has pushed the urgency to create digital solutions for this new financial technology. The Minimalist has proposed some suggestions to help create a smooth user experience by utilizing personalization, data visualization, security, and more.

Introduction.

Defining Central Bank Digital Currency

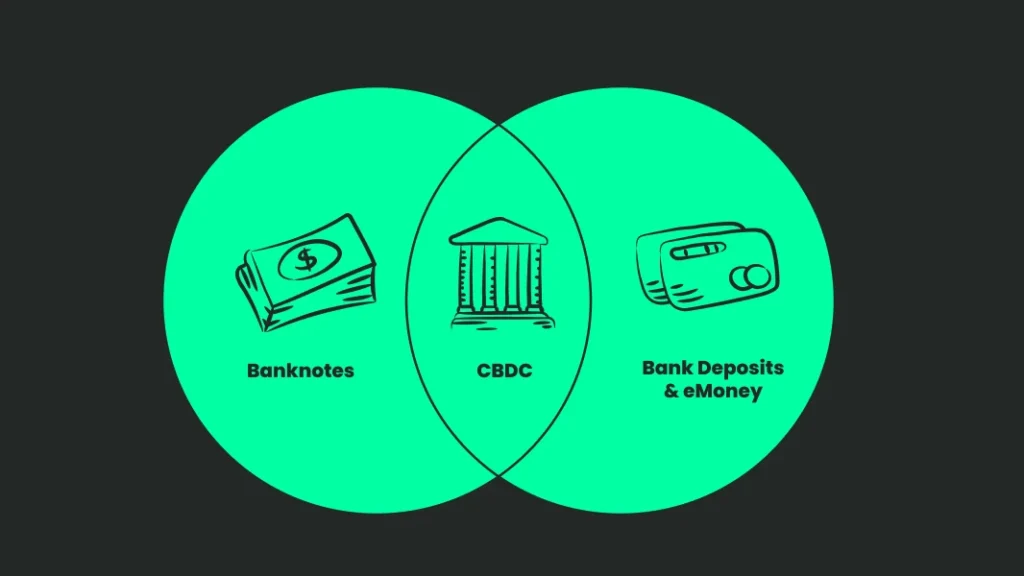

Central Bank Digital Currency (CBDC) is a digital variant of money issued by a central bank, similar to banknotes and coins which could be used by businesses and households to make payments and as a store of value. CBDC is a fiat currency and not backed by any commodities like silver and gold. Below shows how CBDC would be a universally accepted and accessible form of money issued by the Central Bank.

The Reserve Bank of India (RBI) has defined CBDC as, “the legal tender issued by a central bank in a digital form”. The main features of the CBDC described by RBI are its similarity to fiat or sovereign currency, and its greater accessibility and acceptance due to the given similarity. The RBI also ensures that CBDC will resonate with the core functions of the fiat currency as they will be used in making transactions, as legal tender, or as a means to safely store value.

A CBDC has a combination of digital ledger technology and cryptography to offer this electronic variant of cash. It is a central bank’s liability to issue as a central bank reserve (if held by financial intermediaries) and mimic characteristics of physical cash (if held by individual users).

A central bank’s core function is to provide financial stability and monetary stability. The CBDC would create new opportunities and affect them in two ways.

Current monetary system and payments. CBDC would be expressed in the form of money units like Euros, Dollars, Yen, and other similar worldwide currencies and have the same equation as banknotes and coins.

It may have monetary units of 10, 50, 100, 500, and 1000 like physical banknotes and coins. The central bank will require a new configuration to issue CBDC and make transactions digitally. CBDC has to consider two factors to make this possible

- Database to register CBDC.

- An application to execute transactions of CBDC

CBDC can be used to exchange services and goods and can also be considered legal tender. Since COVID-19, we have seen a vast increase in the use of digital transactions. Moreover, the latest technologies have allowed financial institutions and governments to provide a credit-based platform in which balances and transactions are recorded digitally.

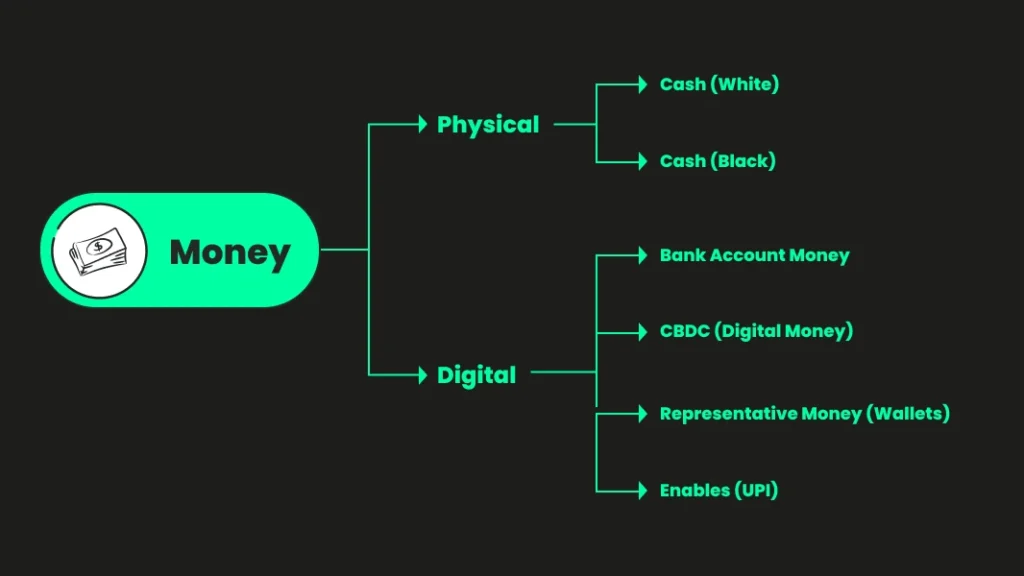

How does CBDC vary from physical cash?

Cash offers great convenience, is usable, easy to store, and is highly popular worldwide. It is difficult to measure a country’s progress from cash to digitization considering the fact that cash has a high degree of anonymity. It is challenging to measure the exact amount of transactions and the worth of such transactions. CBDC is a digital version of the Rupees kept in your wallet. Storing and transacting with CBDC would be more efficient and convenient than physical cash.

Centralized and Decentralized ledger systems

Technology consideration shall always remain CBDC’s base; it is digital and the selection of the technology depends upon several factors like sound technical administration, technical stability, and flexibility. CBDC would require a large-scale digital platform hence careful planning is required. On account of these many factors, CBDC should be configured like the functionality of economy, reduce frauds, decentralization for effective participants amongst users, authentication, data integrity, high volume of currency, rate of transactions, design for variable workload, and protection from cyber-attacks.

A ledger is a collection of accounts or series of blocks in which account transactions are recorded digitally after suitable verification by the designated authorities.

There are 2 types of ledgers – Centralized & Distributed Ledger.

Centralized Ledger System

A Centralized Ledger System is a collection of all transactions which is controlled and finalized by a single source. A bank is an example of a centralized asset ledger as the bank has total control over the transactions which are published in the ledger, such as a bank statement. If the central authority shuts down suddenly, then all the transactions fail and cannot be processed further and this can lead to misinterpretation of the transaction details in the bank statement. The activity affects all the end consumers. If a bank has the intention of cheating, then the bank can loot the money of all its clients which can cause serious financial loss. The centralized ledger system doesn’t provide restrictions on the activities that can be done by any user on the ledger, as a result, any user can change transaction details on a ledger.

Distributed Ledger System

A Distributed Ledger System is a shared ledger that is not controlled by a single entity. DLT allows recording their details in the system in multiple places and at the same time. A single change to a ledger is reflected in all copies within seconds. Cryptography maintains the accuracy and security of the assets stored in the ledger. The assets can be financial, physical, legal, or electronic. It is a fast-developing approach and allows sharing across the ledger (multiple data storage) that have the same data records The ledgers are controlled and maintained by multiple computer servers (nodes).

If a location suddenly shuts down, the remaining locations have the capacity and enough data to maintain the ledger in case of unavailability of the non-working location. That’s how DLT decreases errors and provides real-time information on transactions.

What is Blockchain?

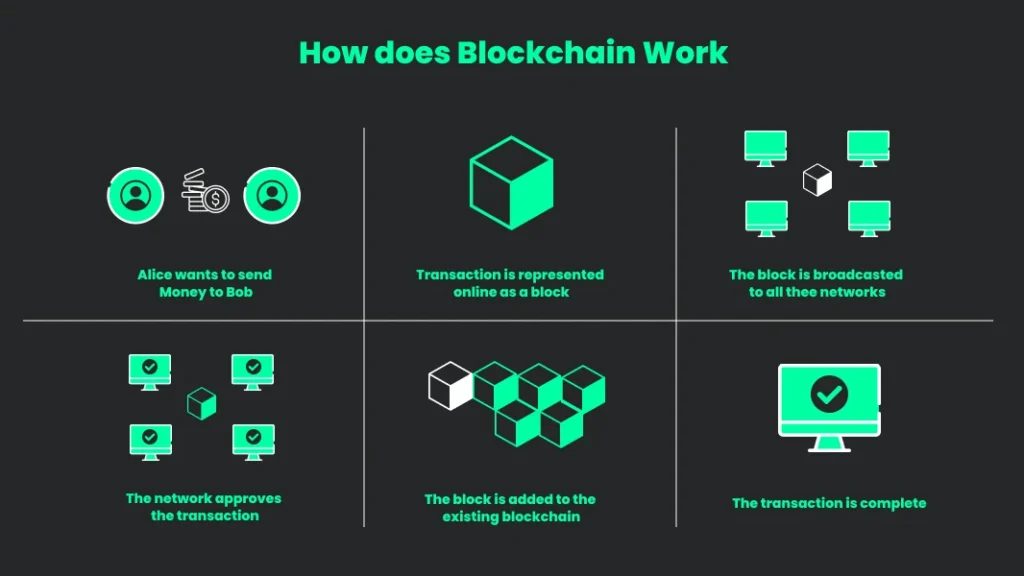

Blockchain is one type of Distributed Ledger System. Blockchain is an advanced database system for recording information in a manner that makes it hard to cheat or hack the mechanism. The popularity and success of Bitcoin made blockchain a trending technology in the world. The technology would be helpful in finance, healthcare, education, and many other sectors.

Blockchain applies methods of algorithm and cryptography to create and verify constantly growing data structures that create a chain of blocks or transaction of blocks that works as a ledger. In multiple computers, all the transactions are recorded with the help of a decentralized public ledger. A record of a new transaction is added as a new block to the chain whenever a new transaction occurs. After performing an authenticity check of the transaction the new block is added to every participant’s node ledger.

Approach

Implementation of CBDC

BIS (2020) highlighted risks associated with the issuance of CBDC that affects financial stability and negatively impacts the monetary system. Hence, BIS adopted a risk-based approach and mentioned three basic and important principles for a central bank to issue CBDC.

- It should be aligned with public policy.

- It should co-exist with the current form of money.

- It should increase the work efficiency of the payment system through competition and innovation.

There are two ways to implement CBDC in the current Monetary system.

- Single tier method

- Two-tier method.

Direct (Single-tier model)

In a direct implementation, the central bank makes it possible to issue CBDC directly to everyone. Community banks and informal gig workers can also deposit their money directly with the bank. In this method, a Central bank would be responsible for all aspects of the banking system like account keeping, issuance of money, and verification of transactions.

Indirect (Two-tier model)

In an indirect implementation, the Central bank indirectly issues CBDC to the end users through an intermediary layer. The layer would be commercial banks to constitute a claim like wholesale and retail payment. The central bank keeps an eye on the bulk balance of the intermediaries rather than end users and the bank has to make sure that the wholesale balance with intermediaries is equal to the retail balance of the end users.

Hybrid (Two-tier model)

In the Hybrid implementation, an intermediate or payment service provider represents a claim along with a direct claim on the central bank. Central banks issue CBDC to other financial authorities and make those entities responsible for direct transactions to the end consumers. RBI can develop and issue tokens to the authorized (Token Service Provider) entities issued in form of tokens who later distribute amongst end users who engage in retail activities.

Adoption of Graded Implementation of CBDC in India

The main aim of the RBI is to maintain monetary and financial stability and to create efficient and secure payments. India is ahead of many countries in terms of innovation in digital payments. The Reserve Bank will be able to adopt the method of proof of concept, pilots, and launch to implement a graded approach CBDC. The motivation behind issuing CBDC in India includes financial inclusion, trust, security, integrity, resilience, and innovation in the payment system.

The design of CBDC should be aligned with financial stability, efficient operations of payment systems and currency, and the stated objectives of monetary policies. The RBI will use Blockchain and other advanced technologies to make CBDC safe from cyber attacks.

As CBDCs are intended to mimic the sovereign or fiat currency issued by the government, the goal behind implementing this financial change is to bring further ease to the system. The RBI aims for CBDC to showcase the same features that are associated with fiat currency by the users. Some “key motivations” identified for launching the CBDC in India include the reduction of operational costs that come with printing fiat currency, enhancing financial inclusion and accessibility, incorporating innovation in the system, easing cross-border transaction experience, and allowing the public to experience the benefits of digital currencies without the attached risks seen in the case of cryptocurrencies (PIB, 2022).

Types of CBDC

India has exhibited primacy in digital payment innovation. The latest payment methods are available 24 hours, a to both retail and wholesale consumers. The payment systems have the lowest transaction cost and are working effortlessly day and night.

CBDC can be classified into two broad categories

- Retail CBDC (Individual users and retailers)

- Wholesale CBDC (Rare financial institutes and some banks)

Retail CBDC

Targeted and are made for the general public to increase features like accessibility, availability, and traceability, and the main functionality is to support and ease daily financial transactions. With the aim of having greater accessibility, CBDC will allow users with no bank accounts and/or limited network connectivity to obtain and conduct transactions with this digital currency, at a lower transaction cost due to limited interference from intermediaries. Retail CBDC is a direct liability of the Central Bank and provides benefits of settlement and gives safe money for the payments.

Wholesale CBDC

Focused on increasing the efficiency of payments and security of settlements for larger transactions and organizations. A particular aim of the wholesale CBDC is to help users resolve any concerns attached to liquidity and counterparty credit that are normally an area of concern when large transactions are involved. Wholesale CBDC can also offer large retail payment benefits and act as simpler means for settlement systems with real-time and transparent operations. Wholesale CBDCs are highly suitable for central banks in advanced economies, exchanging or trading purposes between central and private banks, and other core organizations.

The Indian Ministry of Finance rolled out its curricular or public notice declaring the beginning of the trial phase for CBDC in India by the Reserve Bank of India (RBI). The use cases of wholesale CBDC were limited to “settlement of secondary market transactions in government securities” making them more suitable for complex organizations within the reach of government jurisdiction. The aim of wholesale banking is to improve the overall banking system by reducing transaction costs by minimizing or eliminating the need for intermediary settlement structures like collateral.

The retail CBDC on the other hand was tested with a closed group of users composed of customers and merchants. For retail CBDC, the intention was set clearly as it is meant to take the place of the traditional paper currency or legal tender issued by the bank. Users will be allowed to conduct transactions through digital wallets offered by respective banks which are meant to embody “all the features of physical cash like trust, safety, and settlement finality”.

Goals of CBDC

The main reason or goal to issue CBDC is to ensure end users can access legal tender if cash were unavailable. CBDC may improve the efficiency of the payment system of both retail and wholesale consumers from the point of sale, peer-to-peer, or online. Usage of cash is reducing because of easily available credit cards and easy-to-use and contactless money transaction apps. Cash is difficult to trace to the government so cash becomes vulnerable to tax evasion, money laundering, and illegal transactions.

CBDCs could assist banks to address systemic objectives such as

- Financial inclusion (those who cannot afford or have a bank account)

- Reducing money laundering and fraud

- Promising a dominant substitute for digital payments

- Improve local payments innovation

- Developing a new option for monetary policy.

- Decrease cross-border transaction costs

CBDC’s benefits to businesses and consumers:

- Increase privacy and mobility

- Improve convenience

- Provide financial security and accessibility

Comparison of payment methods

An Indian CBDC should be able to integrate with current payment and transaction methods like UPI, Paytm, digital wallets, etc. The integration should have user adoption, compatibility with other payment methods, and work efficiency which would be helpful to achieve user adoption.

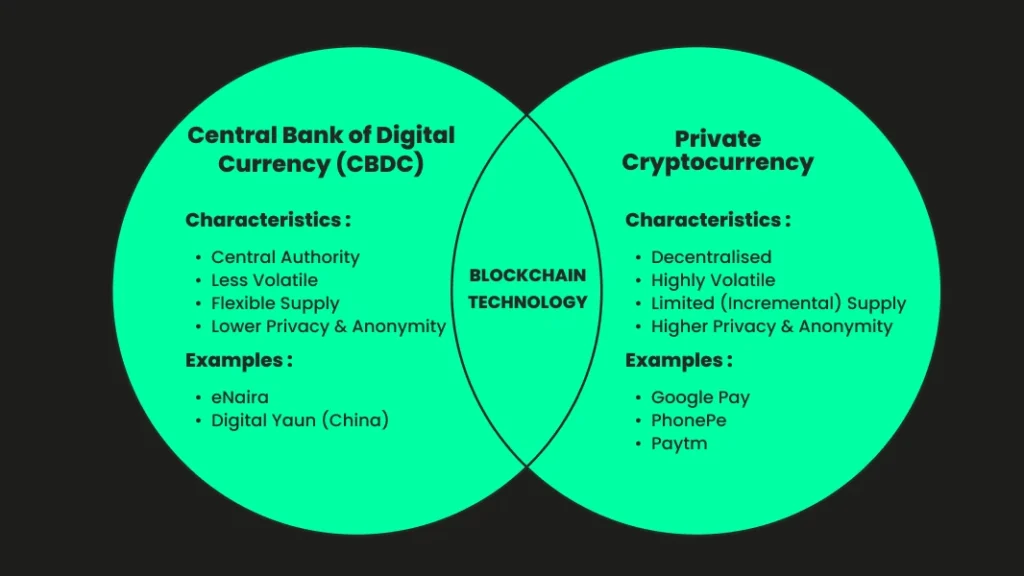

CBDC vs. Cryptocurrency

Crypto is a new experience and it is getting the attention of a larger number of populations worldwide. Crypto is developed as a new technology. The value and efficiency of crypto are not stated, but in the current scenario enact all the functions similar to traditional transaction methods. It is observed that the price and the returns of crypto positively affect user adoption. CBDC is a centralized digital currency that is controlled by the RBI. Hence, CBDC is a legal tender and can be kept in bank accounts, while it may require blockchain technology or advanced mechanisms for security. CBDC represents the value of fiat currency and is designed for stability and safety.

Crypto is decentralized and not connected to or controlled by any government authority and needs to be stored in digital wallets and is hard to duplicate or forge. Crypto is designed to prevent tampering and is dictated by investors’ interests, beliefs, and usage.

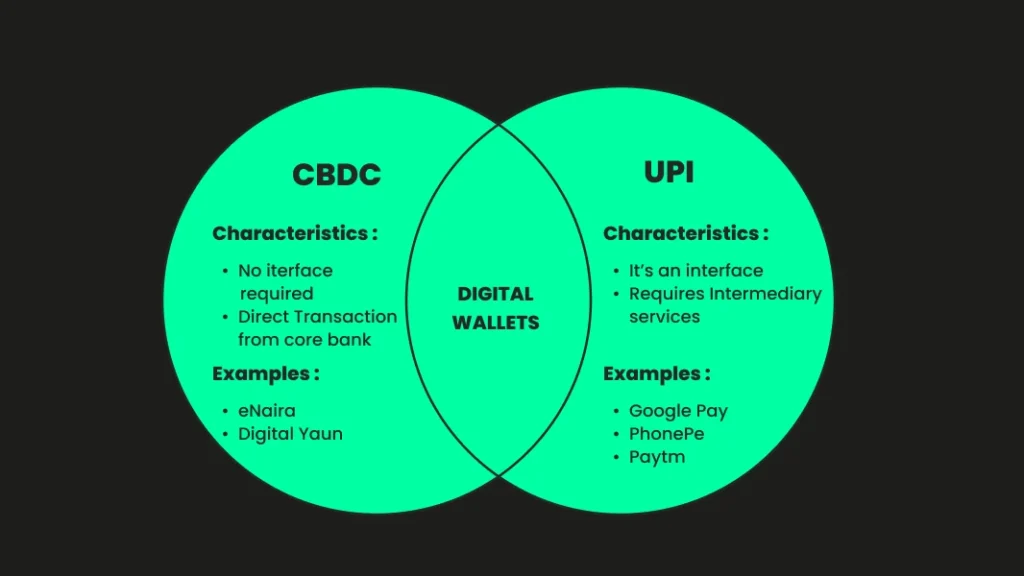

CBDC vs UPI

UPI (Unified Payment Interface) has been employed in India since 2006. The aim of UPI is to provide a platform for online payments, increase financial inclusion, economic development, and effective methods for digitalization in India. UPI works on a technology named open API (Application Programming Interface). Two parties can connect with each other through an open API interface for financial transactions. UPI is a highly accepted payment method in India due to three factors.

- Link with Aadhar card

- Easy to use

- User-friendly app for transactions. Moreover, fintech companies easily integrate with UPI and can provide value-added services.

Digital Rupee is a form of currency similar to fiat currency. In CBDC, when you make a payment to an individual or at a shop, CBDC will move from your wallet to your wallet. You can keep it in your digital wallet as you keep physical currency in your pockets.

In UPI, the transactions occur between two banks or digital wallets to account or account to a digital wallet. UPI is just an interface to make transactions. There is always an intermediation of the bank. While using the UPI app, your bank account gets debited and money gets transferred to the other’s bank account.

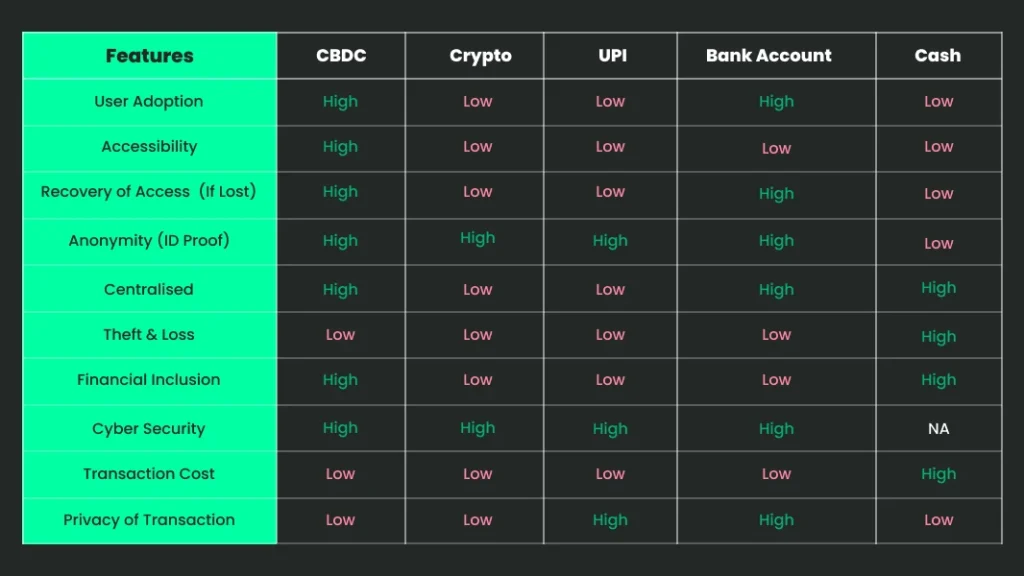

Analysis of different payment methods

To understand the standing of CBDCs amongst other existing forms of payments, we compared them on a range of criteria like user adoption, anonymity, accessibility, security, cost, privacy, etc.

Based on the above table, we can see that CBDCs have higher user adoption owing to their features of increased accessibility to users with or without internet and/or bank accounts, making them more versatile. However, in lower city tiers, attitude could be a hindering factor in adopting new technology without the necessary awareness or education. Therefore, it can be concluded that cash would have higher financial inclusion as it is widely used for a prolonged period of time, gaining the trust of all users. Even though CBDCs are secure due to their blockchain technology that will protect users against malicious attacks, users with higher privacy and security concerns may not openly welcome this shift in the financial system.

Pros and Cons of CBDC

CBDC is a sovereign currency that provides a wide range of advantages like integrity, safety, liquidity and trust for the payment system. The main aim of implementing CBDC in India is to decrease operational costs, enhance financial inclusion, efficiency, and innovation of the payment system, improve efficiency in cross-border transactions, and provide a virtual platform to the general public for daily transactions without any risk.

Pros of CBDC

CBDC enhances financial inclusion for individuals from remote areas or developing countries, low-income individuals, families with unmet necessities, or user groups with no bank accounts. Moreover, CBDC (via central bank) would reduce the financial load caused by the issuance of currencies by tech firms and unions, and will enhance processes and speed of the monetary systems, quick settlements in large values, increase the number of cross-border payments and the ability for central banks to credit household CBDC accounts. It will help the government to influence more money flow in the economy and its borrowing cost which will reduce the popularity of cryptocurrencies due to their volatile nature.

Cons of CBDC

Financial Risks increase in the higher exchange rate and lending costs. CBDC would have lower user adoption from remote areas with limited access to the internet, banking facilities, and relevant awareness. Cyber security risks, vulnerability testing, and costs of protecting the firewalls would be higher for CBDC. Operational risks would be high as the employees have to be re-trained and groomed to work in the CBDC culture. A CBDC can be created in minutes and seconds, which if distributed widely may cause inflation without increasing. Moreover, CBDCs will require large-scale allocation and countrywide infrastructure for distribution and payments as these aspects are required to make CBDCs useful.

Cybersecurity and CBDC

With increasing facilities and advancements provided by technology, many countries have considered digitizing their currencies to make their financial structures more flexible, versatile, and accessible. But with digitization comes the risk of cybersecurity concerns from various ends including the risks from private sectors, end users, and the integrity of the financial system itself. As CBDCs will be public-facing and more open when compared to cryptocurrencies, there would be less threat to end users from the private sector, thus painting CBDC in a positive and achievable light. But on the other hand, the increasing number of cyber warfare attacks can put governments in a tricky position as it could pose a threat to the national financial system.

The World Economic Forum (2021) summarized 4 major cybersecurity threats

Credential Theft and Loss

Access to CBDC will be given in the form of credentials or passphrases which make it more prone to theft as they can be simply communicated through paper or physical tokens. Moreover, the physical devices that store the credentials can be susceptible to manmade or natural disasters, leaving the user’s identity and money vulnerable.

Users with Privileged Roles

Central banks, government insiders, law enforcement, and other agents may have privileged access to information or to actions like freezing or withdrawing funds from users’ accounts. On the other hand, third parties or non-central authorities may accept or reject transactions due to malicious intents, putting the security of end users at risk.

System Integrity and ‘Double Spending’

It is possible for intermediary banks that are not subject to central bank regulation to have powers that might be used maliciously to either invalidate transactions or prevent users from engaging in network activity. Denial-of-service attacks (DDoS) and censorship are consequently caused by this.

Quantum Computing

With the rapid advancement in technology, emerging quantum computing will ultimately impact all financial services as it would revolutionize the way all systems work. It would comprise data encryption methodologies and cryptographic primitives used for protecting access, confidentiality, and integrity of data. This evolution would once again destabilize the financial system, causing more concerns for users who have already adopted CBDC.

In addition to these core concerns, other problem areas will also have to be addressed while designing for CBDC. Centralized data collection can be easily used for citizen surveillance, particularly payment activities, therefore reducing the confidentiality or security behind these transactions. However, this risk can be mitigated either by not collecting or choosing a validation architecture where only the necessary information is seen to validate the transaction. The security guarantee of the ledgers is dependent on third-party vendors whose involvement can be mitigated through regulatory mechanisms such as auditing requirements and stringent breach disclosure requirements. Security concerns have to be kept at the core of designing CBDC as it can soothe the concerns of users with high privacy needs or can be used as a way to establish trust with users with a wavering attitude towards technology and CBDC.

Designing for CBDC

Users and Use Cases

In October 2020, the Bank of International Settlements (BIS) collaborated with several banks the Bank of Canada, the Swiss National Bank, and the Bank of Japan, among others, to understand the core features and foundational principles of CBDC. As there are two broad categories of CBDCs, namely wholesale and retail, the organization found various use cases for different users and scenarios. Several use cases have to be kept in mind while designing CBDCs, which are as stated below:

- Well-connected user with a bank account and options for digital payments

- Users with limited/no internet and from remote areas

- Unbanked users who either do not have a bank account or do desire a bank account

- Users with varied accessibility needs

- Users that prioritize privacy

- Small merchants

To understand the requirements of users, the user stories were defined as “small narrative of a particular user”. User stories aim to convey the user’s goals, tasks to be accomplished, and pain points that may hinder their goal accomplishment. In the case of CBDC, creating user stories will allow us to understand the thoughts, feelings, emotions, and needs of the users at each step of the transaction process or mere interaction journey with CBDC.

Users tend to seek a form of currency or money that will maximize the personal benefits and reduce associated risks and costs. The relative weight of different criteria will vary based on a number of factors such as location, accessibility, attitude towards technological advancements and banking, and cross-border transactions, in addition to some of the use cases mentioned above.

Given below are different use cases that can be uniquely applied to India and the relevant user groups to make CBDC more accessible, approachable, and open to the population.

Programmable Payments (DBT)

CBDC can be used for providing social benefits in other targeted payments in the country, such as the LPG subsidies that can be credited and authorized at LPG agencies and can be further converted to general CBDC or fiat currency at any bank.

Retail payments

Instead of using cards and fiat money, the retail stores can be equipped with specially designed CBDC instruments that will help users make seamless transactions through their wallets or directly to and from the respective bank account of the merchant or the user. This would allow transactions to take place between and among a range of different user groups such as consumers and businesses.

Easier MSME Lending

With direct connection and authentication coming from the bank, drawing accurate borrower risk profiles will become easier, allowing lenders to give more opportunities for MSMEs. Additionally, finances can be easily and directly disbursed without causing any additional transactional or intermediary fees, making borrowing and lending more accessible and affordable. Moreover, the traceability of CBDC in the central system can add to the creditworthiness and transparency which can furthermore increase its resiliency to forgery and financial misconduct.

Offline Payments

The design of CBDC would include an offline wallet based on Near-Field Communication (NFC)-abled devices to allow users with weak or no network to make payments that will be enabled as soon as a secure internet connection gets established.

Some other wide ranges of use cases involve payment settlements between businesses, using CBDCs as a way of identity management for security concerns, cross-border payments, and asset transfers.

The key point to consider while designing CBDC

As CBDCs aim to replace fiat currency or sovereign currency, they should be able to present all the features, characteristics, and advantages that come with physical currency. The design of CBDC is highly reliant on the functions it is expected to perform by various user groups and how the design impacts or alters the existing payment systems, and policies, as well as the structure and stability of the financial system.

The Bank of International Settlements (BIS) (2020) followed a risk-based approach in an effort to identify potential risks, specifically the risks that can overturn financial stability or impact financial market structures. The considerations are given as follows:

- It should have a “do no harm” policy, i.e., it should not hinder public policy or cause any turbulence for the stability of the banking systems.

- It should coexist with the current forms of transactions and currencies allowing the users more opportunities and freedom to opt for their preferences.

- CBDC should be a means of promoting innovation and technological advancement with the main purpose being increasing accessibility for users.

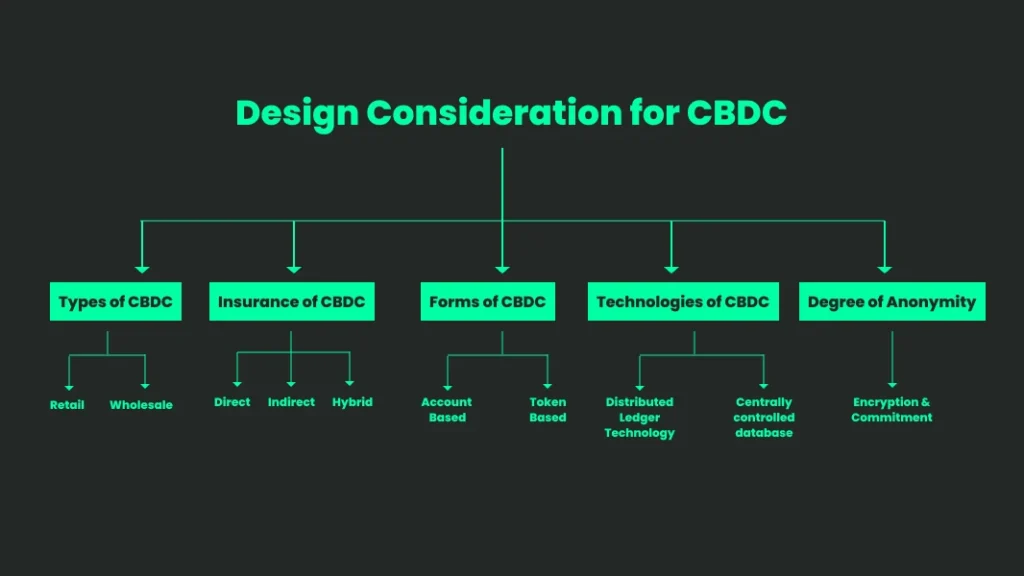

In an article published by the Reserve Bank of Australia (2020), the authors suggest certain design considerations that need to be accounted for while developing CBDCs. The paper elaborates on how account-based CBDCs would require a separate ledger to keep track of the transactions made by users and merchants and would ensure the transfer of CBDC balances from one account to another, while in the case of a token-based CBDC, it would closely simulate the current system where a token represents a “claim” of the central bank. Looking at this classification also poses the question of the degree of security of CBDCs. Account-based CBDC may have lesser security due to the maintenance of a detailed ledger, thus lowering the anonymity of the transactions. There are options available for intermediate privacy in the form of “privacy vouchers” as tested by the European Central Bank (2019) to provide the users with complete anonymity for smaller transactions while larger transactions will be visible to the government. Yet another design consideration for CBDC would be to determine the best technology behind the innovation. Though the Bank of England (2020) suggests the use of Distributed Ledger Technology (DLT) owing to its high resilience and availability, the drawbacks of this system are largely focused on the retail segment where the unavailability of a payment system is often a concern. DLT could negatively impact essential user requirements such as performance, privacy, and security.

Examples: eNaira (Nigeria)

eNaira is a Central Bank of Nigeria-issued digital currency that provides a unique form of money denominated in Naira.

In their effort to improve accessibility, eNaira’s background research illustrates how the government has considered several factors allowing direct disbursements of welfare to citizens, facilitating diaspora remittances, and improving the ease of cross-border transactions while reducing the additional costs. They aim to enable and empower each individual or community to make reliable, safe, and efficient payments while reaping the benefits of innovation, inclusion, and accessibility through their design. eNaira also employs the three general principles laid down by the BIS and further expanded them to suit the native needs by incorporating principles like inclusivity, innovation, efficiency, resilience, and a product that is proudly Nigerian. They also took into consideration the World Economic Forum and BIS to establish their architecture of using a “hyper ledger fabric variant” of DLT and other design principles for interoperability, accessibility, and security for users

Examples : Digital Yuan – eCNY (China)

The Deutsche Bank conducted research to understand the e-CNY or the Digital Yuan published by the Public Bank of China (PBOC). The PBOC, central bank, and e-CNY officials have conducted several pilot tests to check for adoption, accessibility, and general attitude of users towards the CBDC.

Some of the goals for the CBDC as noted by the Deutsche Bank research were as follows

- A long-term goal was to create a currency that is widely accepted across the globe and has a place in the market similar to other digital currencies. This long-term goal of establishing the digital currency was made in accordance with the design principle that states that the introduction of CBDC should not create an imbalance in the existing financial system and should rather be treated as an additional option for the users to make transactions.

- The more immediate short-term goal observed was to “reshape China’s current payment systems”, by presenting a more accessible and versatile method of payment at low cost and security risks.

The Public Bank of China, in its e-CNY design paper, has established the design considerations for the CBDC and incorporated its framework for both the operating system as well as the e-CNY wallet. The e-wallet can be personal or corporate, software or hardware, and a parent or sub-wallet based on the type of holder, carrier, and authorization respectively. They have also highlighted the principles behind the development of CBDC, which are compliance with laws and regulations, safety and convenience, and openness and compatibility. Drawing from the works of BIS and the models proposed by other governments across the globe, the e-CNY also has features like flexible identity as an account-based or value-based system, non-interest accrual, low cost, settlement upon payment, managed anonymity, safety, and programmability.

The Minimalist’s design perspective

Traditionally, design has been thought of as an eye-catching marketing tool used to entice customers to purchase a product. Historically, financial products were also complex and difficult to comprehend. In recent years, there has been a shift in focus to creating rich user design experiences as users become more intuitive when navigating the digital world. Financial institutions, for example, are increasingly realizing the importance of providing their customers with feature-rich mobile banking applications that are easy to navigate and use. Banks will struggle to improve customer satisfaction and win the hearts of digital natives unless they provide a seamless digital banking experience. A study from Chase bank shows that 99% of Gen Z and 98% of Millennials use mobile banking apps. According to research, users now spend 10.8 times more time on FinTech applications, which are typically designed with user experience in mind, than on traditional banking applications. This has made it clearer than ever, that user-centricity should be at the forefront of design. Customer centricity means users expect a more ethical, responsible, and honest attitude from banks and their products. Transparency and content simplification go a long way toward achieving customer-centricity.

Our process at The Minimalist aligns and expands on this avenue of user-centricity by combining business needs and user needs to create a thoughtful, impactful, delightful, and innovative experience.

The Minimalist’s experience design and technology department has translated their expertise in designing digital products across financial services like insurance, banking, and payments to the emerging CBDC/digital rupee concept. Some design suggestions for a successful experience are listed below:

Personalization

Personalisation uses user behavior data and machine learning to deliver content and functionality that is tailored to a user’s specific needs or interests. Personalization is implicit — it is controlled by the system and does not require the user’s conscious input or effort. Users are profiled individually and content is tailored to each individual user (simple experience to Netflix, Spotify, or Instagram).

Security

Consumers today demand biometric features such as fingerprint and facial authentication. Offering the most up-to-date security improves user experience while also fostering user confidence. Over the next 10 years, businesses should concentrate on developing new techniques for detecting fraud, monitoring activities and potential risks in real-time, and expanding the availability of services online.

Intuitive, Delightful Designs

The inherent appeal of digital finance is the ease of use, but it cannot be so effortless that it is easy for users to make mistakes with their money.

- Prioritization of content

- Sequence information and actions

- Using common patterns (Jakobs Law)

Data Visualisation

Users will adore dashboards with tables and graphs offering condensed financial data. If you want to greatly enhance the experience of your users, it is worthwhile to incorporate this trend into your application.

Navigation and System Status. While Gen Z and Millenials are digital natives while designing a service we need to cater to a larger audience. Communicating the current status allows users to feel more in control of the system, take the appropriate actions to reach their goals, and ultimately build trust in the brand. Communication increases trust, one of the key elements impacting customer retention.

Summary and Conclusion

As economies become increasingly digital, user needs and demands have evolved over the period, and launching CBDCs would have to follow the steps in order to meet the user needs. The Central Bank could accommodate evolving user needs by designing a flexible core system and integrating a diverse ecosystem of intermediaries delivering choice, competition, and innovation. The weight of the different factors at play in determining whether users would adopt and use CBDCs would largely depend on the public policy objectives and future market conditions in each jurisdiction. CBDC would fulfill all the needs, goals, and requirements and ease the pain points of end users, and one day it will take the place of “physical currency”. Given the foundation and goals of the CBDC established by the central government, there can be immense opportunities to design interfaces for user-facing and B2B platforms for CBDC wallets, transactions, and much more. There is great scope for design principles and specialists to prioritize user needs, use cases, and government goals and innovate designs that can make the transition from traditional to digital currency much easier for the users.